Selling a second home can trigger a significant capital gains tax liability. This tax is levied on the profit you make from the sale. The good news is that there are several strategies you can employ to reduce or even eliminate this tax. Can you avoid capital gains tax on a second home entirely? In some situations, yes. This article delves into expert-backed methods for minimizing your capital gains tax when selling a second home, ensuring you keep more of your hard-earned profits.

Image Source: www.financestrategists.com

Deciphering Capital Gains Tax on Second Homes

When you sell a property for more than you paid for it, that profit is considered a capital gain. The IRS taxes these gains. For second homes, which are not your primary residence, this tax typically applies to the entire profit. The rate of this tax depends on your income bracket and how long you owned the property. Short-term capital gains (on assets held for one year or less) are taxed at ordinary income rates, which are generally higher. Long-term capital gains (on assets held for more than one year) are taxed at preferential rates, currently 0%, 15%, or 20%, depending on your taxable income.

It’s crucial to understand your holding period. This is the length of time you owned the property. A longer holding period generally means a lower tax rate on your gains.

Key Factors Influencing Your Capital Gains Tax

- Purchase Price: What you initially paid for the property.

- Sale Price: The price at which you sell the property.

- Improvements: Costs incurred for significant upgrades and renovations that add value to the property.

- Selling Expenses: Costs associated with selling, such as real estate commissions, legal fees, and closing costs.

- Holding Period: How long you owned the property.

Strategies for Capital Gains Deferral and Reduction

There are various proactive approaches to real estate tax planning that can significantly impact your capital gains tax liability on a second home. These strategies range from leveraging existing tax laws to making strategic financial decisions before and during the sale.

1. Maximizing Your Cost Basis

Your cost basis is essentially what you invested in the property. The higher your cost basis, the lower your taxable capital gain.

Adjusting Your Cost Basis

- Original Purchase Price: This is the starting point.

- Closing Costs: Include expenses paid at the time of purchase, such as title insurance, legal fees, appraisal fees, and recording fees.

- Capital Improvements: These are permanent additions or significant upgrades that add value to the property or extend its useful life. Examples include:

- New roof or HVAC system

- Major kitchen or bathroom renovations

- Adding a swimming pool or deck

- Landscaping that significantly enhances the property’s value

- Installing a new fence or driveway

- Certain Assessments: Homeowners association or property assessments for capital improvements can sometimes be added to your basis.

What Doesn’t Increase Your Cost Basis?

- Repairs: Routine maintenance and minor repairs, like fixing a leaky faucet or repainting a room, do not increase your cost basis.

- Costs of Selling: These are typically deducted from the sale price, not added to the cost basis.

Example:

Let’s say you bought a second home for \$300,000 and spent \$50,000 on a new kitchen and \$20,000 on a new roof. You also paid \$10,000 in closing costs when you bought it. Your adjusted cost basis would be \$300,000 + \$10,000 + \$50,000 + \$20,000 = \$380,000. If you sell it for \$500,000, your capital gain is \$500,000 – \$380,000 = \$120,000.

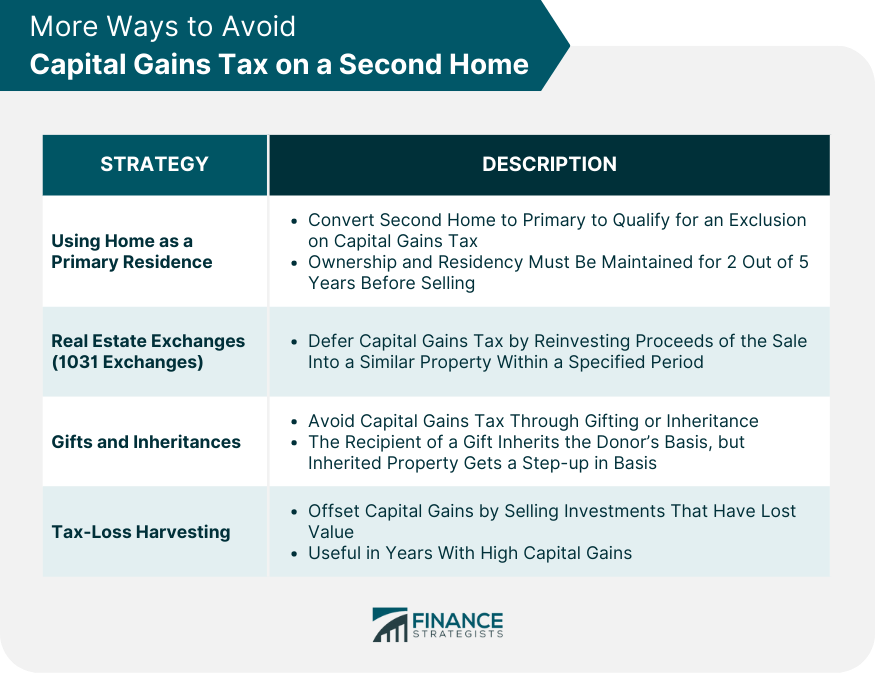

2. The Primary Residence Exclusion: A Limited Option

The primary residence exclusion allows homeowners to exclude a certain amount of capital gain from the sale of their home if it was their principal residence. For single filers, this exclusion is up to \$250,000, and for married couples filing jointly, it’s up to \$500,000.

Can You Use the Primary Residence Exclusion on a Second Home?

Generally, no. This exclusion is strictly for your primary residence. To qualify, you must have owned and lived in the home as your main home for at least two out of the five years leading up to the sale.

However, there’s a nuance: if you used to live in the second home as your primary residence and then moved out, you might be able to utilize a portion of the exclusion. If you lived in the home for two years and then rented it out for less than three years, you may still be able to claim part of the exclusion on the gain that accrued during the time you lived there. However, gains accrued during the rental period would be taxable. This is a complex area, and consulting a tax professional is highly recommended.

3. Rental Property Depreciation: A Double-Edged Sword

If you’ve rented out your second home, you’ve likely taken rental property depreciation deductions. Depreciation allows you to deduct a portion of the property’s value each year, reducing your taxable income during the rental period. This is a valuable tax benefit.

The Depreciation Recapture Tax

The catch is that when you sell the property, the IRS requires you to “recapture” the depreciation you claimed. This means the portion of your gain attributable to depreciation is taxed at a special rate, typically up to 25%.

Example:

If you claimed \$50,000 in depreciation over the years, and your total capital gain is \$120,000, then \$50,000 of that gain will be taxed at the depreciation recapture rate, and the remaining \$70,000 will be taxed at the standard long-term capital gains rates.

Strategies to Mitigate Depreciation Recapture

- Hold Longer: The longer you hold the property, the more your basis is adjusted by depreciation, but the overall gain is also spread out over a longer period, potentially benefiting from lower long-term capital gains rates on the non-depreciation portion.

- Improve the Property: Continuing to make capital improvements can increase your cost basis, offsetting some of the gain, including the portion subject to depreciation recapture.

4. The 1031 Exchange: Deferring Taxes Through Real Estate Swaps

One of the most powerful strategies for avoiding capital gains tax on investment properties, including second homes that function as rentals, is the 1031 exchange, also known as a like-kind exchange.

What is a 1031 Exchange?

A 1031 exchange allows you to defer capital gains taxes by reinvesting the proceeds from the sale of one investment property into another “like-kind” investment property. The key is that the replacement property must be of equal or greater value, and you must adhere to strict timelines.

How a 1031 Exchange Works:

- Sell Your Relinquished Property: You sell your second home.

- Engage a Qualified Intermediary (QI): You cannot receive the sale proceeds directly. A QI holds the funds in a qualified escrow account.

- Identify Replacement Property: Within 45 days of selling your relinquished property, you must formally identify potential replacement properties. You can identify up to three properties of any value, or any number of properties as long as their total fair market value doesn’t exceed 200% of the relinquished property’s value.

- Acquire Replacement Property: You must close on the purchase of the replacement property(ies) within 180 days of selling your relinquished property. The replacement property must be of “like-kind,” meaning it’s also held for investment or productive use in a trade or business. For real estate, this generally means any type of real estate held for investment purposes qualifies as like-kind.

Key Considerations for a 1031 Exchange:

- Investment Property: The 1031 exchange is only for investment or business properties, not personal residences. Your second home must have been used as a rental or for business purposes to qualify.

- Like-Kind: As mentioned, most real estate qualifies as like-kind to other real estate.

- Equal or Greater Value: To defer all capital gains tax, the replacement property must be of equal or greater value than the relinquished property. If the replacement property is of lesser value, you will pay tax on the portion of the gain that is not reinvested.

- Financing: If you use a mortgage to buy the replacement property, it counts as “boot” and can trigger a partial tax liability. It’s advisable to use cash or offset the equity difference with cash to avoid boot.

- Depreciation Recapture: A 1031 exchange defers the tax on the entire gain, including the portion attributable to depreciation. However, the deferred depreciation is added to the basis of the new property, meaning you’ll face depreciation recapture tax when you eventually sell the replacement property without another exchange.

Table: 1031 Exchange Timelines

| Step | Deadline |

|---|---|

| Sell Relinquished Property | Start of the 1031 Exchange process |

| Identify Replacement Property | No later than 45 days after the sale of the relinquished property. |

| Acquire Replacement Property | No later than 180 days after the sale of the relinquished property, or the due date of your tax return (including extensions), whichever is earlier. |

| QI Holds Proceeds | Must be held by the QI from the sale of the relinquished property until the purchase of the replacement property. |

5. Selling a Second Home Over Time: Installment Sales

An installment sale allows you to receive payments for the sale of your second home over several years. This can spread out your capital gains tax liability, potentially placing you in a lower tax bracket in the years you receive payments.

How Installment Sales Work:

- Contract: You and the buyer agree to an installment sale contract.

- Payments: The buyer makes payments over a period of time, including interest.

- Tax Reporting: You report the portion of the gain received in each tax year.

Benefits of Installment Sales:

- Tax Deferral: You defer paying tax on the gain until you receive payments.

- Lower Tax Rates: By spreading income over multiple years, you might avoid higher tax brackets.

Drawbacks of Installment Sales:

- Interest Income: The interest portion of the payments is taxed as ordinary income, not capital gains.

- Buyer Financing: You become the lender, which carries risks if the buyer defaults.

- Depreciation Recapture: Any depreciation recapture must be recognized in the year of the sale, regardless of when payments are received.

6. Tax-Loss Harvesting: Offsetting Gains with Losses

Tax-loss harvesting is a strategy where you sell investments that have decreased in value to offset capital gains. While typically associated with stocks and bonds, it can also be applied to real estate in certain situations.

Applying Tax-Loss Harvesting to Real Estate:

- Other Investment Losses: If you have other investment assets (like stocks or mutual funds) that have experienced losses, you can use those losses to offset capital gains from the sale of your second home.

- Limited Real Estate Application: It’s rare to “sell” a property at a loss specifically for tax-loss harvesting purposes unless it’s a non-performing investment property you’re eager to divest. The transaction costs and complexities of selling real estate often make this impractical compared to selling securities.

How it Works:

- Capital losses can offset capital gains dollar-for-dollar.

- If your capital losses exceed your capital gains, you can deduct up to \$3,000 of the excess loss against your ordinary income each year.

- Any remaining net capital loss can be carried forward to future tax years.

7. Timing Your Sale Strategically

The holding period is critical for determining whether your gain is short-term or long-term. Selling after you’ve owned the property for more than one year can significantly reduce your tax rate on the profit.

Holding Period Impact:

- Owned for 1 year or less: Short-term capital gains, taxed at ordinary income rates.

- Owned for more than 1 year: Long-term capital gains, taxed at lower rates (0%, 15%, or 20%).

If you’re nearing the one-year mark, it might be beneficial to delay the sale to qualify for the lower long-term capital gains rates.

8. Structuring the Sale: Renting vs. Selling

If your second home is currently a rental property, consider the advantages of continuing to rent it out versus selling it.

Factors to Consider:

- Cash Flow: Does the property generate positive cash flow after expenses?

- Appreciation Potential: Do you anticipate further appreciation in value?

- Tax Benefits of Ownership: The ability to continue claiming rental property depreciation and deducting operating expenses can still provide tax advantages.

- Market Conditions: Are current market conditions favorable for selling?

If the property is not performing well financially and you’re facing a large capital gains tax bill, selling might be the right move, but a strategic approach is essential.

9. Using a Donor-Advised Fund (DAF) for Charitable Giving

If you are charitably inclined, you can donate your second home to a qualified charity or a Donor-Advised Fund (DAF).

Benefits of Donating Property:

- Avoid Capital Gains Tax: When you donate appreciated property to a public charity, you generally do not owe capital gains tax on the appreciation.

- Charitable Deduction: You can typically deduct the fair market value of the donated property (up to certain AGI limits) on your tax return.

Important Considerations:

- Appraisal: You’ll need a qualified appraisal to determine the fair market value.

- Charity’s Acceptance: Ensure the charity is willing and able to accept the property. Some charities may not want the burden of managing real estate.

- Holding Period: The property must have been held for more than one year to qualify for the deduction of the fair market value. If held for one year or less, your deduction is limited to your cost basis.

Frequently Asked Questions (FAQ)

Q1: Can I exclude capital gains from a second home sale if I never lived in it?

Generally, no. The primary residence exclusion is specifically for the home you lived in as your principal residence. For investment properties like a second home you’ve always rented out, this exclusion does not apply.

Q2: What is the difference between a 1031 exchange and the primary residence exclusion?

The primary residence exclusion is a one-time exclusion on the sale of your main home, allowing you to exclude up to \$500,000 in gains (for married couples). A 1031 exchange is a method of deferring capital gains taxes on investment or business properties by reinvesting the proceeds into a like-kind property. It does not eliminate the tax but postpones it.

Q3: How do I calculate my capital gain?

Your capital gain is calculated as the selling price minus your adjusted cost basis. Your adjusted cost basis includes the original purchase price, closing costs from the purchase, and any capital improvements made. You also subtract selling expenses (like realtor commissions and closing costs from the sale) from the selling price before calculating the gain.

Formula:

Capital Gain = (Selling Price – Selling Expenses) – (Original Purchase Price + Purchase Closing Costs + Capital Improvements)

Q4: What are the tax implications of selling a vacation home I used personally but also rented out occasionally?

If you rented out the second home for 15 days or more during the year, you must report rental income. If you also used the home personally, you can only deduct rental expenses up to the amount of rental income. Additionally, you may need to prorate certain expenses and depreciation deductions based on personal use versus rental use. When selling, gains accrued during the rental periods are taxable, and you’ll also face depreciation recapture on any depreciation claimed. The primary residence exclusion generally won’t apply if it wasn’t your main home.

Q5: Is it better to sell a second home now or wait?

This depends on several factors: your holding period (to qualify for long-term capital gains rates), current market conditions, your personal financial situation, and potential tax law changes. If you’re close to the one-year mark for long-term capital gains, waiting might be beneficial. If you have significant other capital losses, tax-loss harvesting could make selling now more advantageous. Consulting with a tax advisor is crucial for making this decision.

Expert Tips for Seamless Real Estate Tax Planning

Navigating the complexities of capital gains tax on second homes requires careful planning and an awareness of available strategies. Here are some final expert tips:

- Document Everything: Keep meticulous records of all purchase-related costs, capital improvements, and selling expenses. This is vital for accurately calculating your cost basis and minimizing your taxable gain.

- Consult a Tax Professional Early: Don’t wait until the last minute. Engage a qualified CPA or tax advisor well in advance of your sale. They can help you assess your situation, explore all applicable strategies, and ensure compliance with IRS regulations.

- Consider Your Exit Strategy: When purchasing a second home, think about your long-term plans. If you intend to sell it later and want to defer taxes, a 1031 exchange might be a consideration from the outset, especially if you plan to invest in other real estate.

- Evaluate Your Entire Portfolio: When planning real estate tax planning, consider your entire investment portfolio. Losses from other investments can be used to offset gains from your second home sale through tax-loss harvesting.

- Understand Depreciation Recapture: Be aware that depreciation claimed on rental properties will be taxed at a specific rate upon sale. Factor this into your calculations.

- Prioritize Primary Residence Exclusion: If a second home might someday become your principal residence, meticulously document your living arrangements to potentially qualify for the exclusion down the line, adhering to the ownership and use tests.

By implementing these strategies and seeking professional guidance, you can effectively manage and potentially avoid significant capital gains tax liabilities when selling a second home, preserving more of your investment’s profit.