What is a mortgage appraisal and can it impact my home loan? A mortgage appraisal is a key step in obtaining a home loan. It’s a professional, unbiased opinion of your home’s market value. This real estate assessment plays a crucial role in how much a lender will loan you. It helps determine the property value, influencing your loan-to-value ratio and ultimately your mortgage approval.

Image Source: www.directmortgageloans.com

The Crucial Role of Home Valuation in Your Loan Journey

Securing a home loan is a significant financial undertaking, and at the heart of this process lies the home valuation, commonly known as a mortgage appraisal. This isn’t just a formality; it’s a critical determinant of your borrowing power and the terms of your mortgage. Lenders rely heavily on this independent assessment to mitigate their risk, ensuring that the property they are financing is worth the amount they are lending. Without a solid appraisal, your dream of homeownership might face unexpected hurdles.

Deciphering the Appraisal Process: What Happens

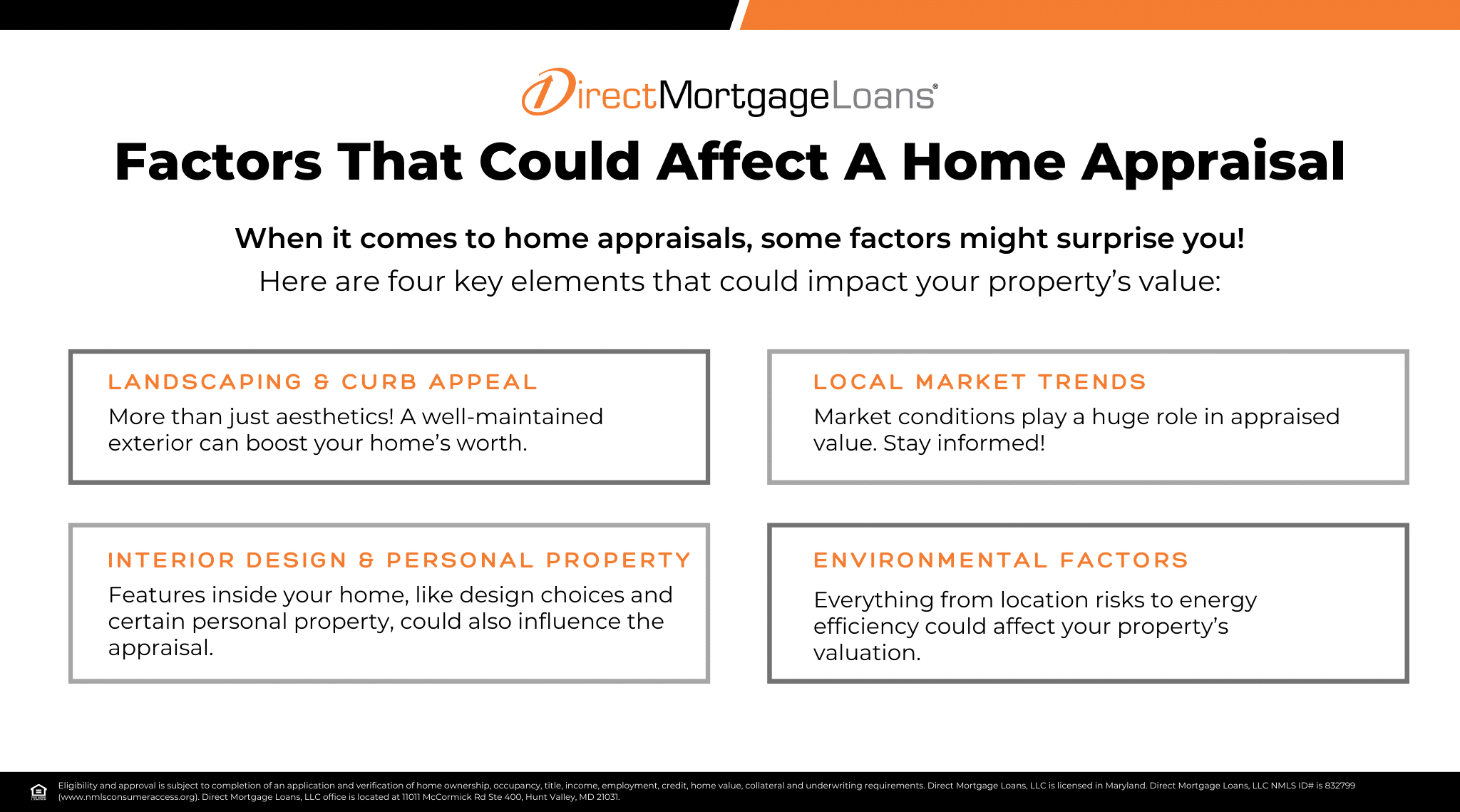

The appraisal process involves a licensed or certified appraiser meticulously examining your property. They don’t just look at the house; they consider various factors that contribute to its overall property value. This includes the home’s condition, size, features, and any recent renovations. Crucially, they also analyze recent sales of comparable properties in your neighborhood. These “comps” are properties that have sold recently and share similar characteristics to yours. The appraiser uses this data to establish a fair market value for your home.

Key Elements Evaluated by Appraisers:

- Location: Proximity to amenities, schools, and desirability of the neighborhood.

- Size and Square Footage: The overall living area and lot size.

- Condition of the Property: This includes the structural integrity, roofing, plumbing, electrical systems, and overall maintenance.

- Features and Amenities: The number of bedrooms and bathrooms, kitchen and bathroom quality, presence of a garage, backyard, or special features like a swimming pool.

- Updates and Renovations: Recent upgrades to kitchens, bathrooms, flooring, or energy-efficient systems can significantly boost value.

- Comparable Sales (Comps): The most important factor, this involves analyzing the sale prices of similar homes in the immediate vicinity that have sold within the last six months.

- Market Trends: The appraiser considers the current real estate market conditions in your area. Is it a buyer’s market or a seller’s market?

Why Lenders Require Appraisals: Protecting Their Investment

Lenders aren’t in the business of taking on excessive risk. When you apply for a home loan, the lender is essentially purchasing your promise to repay the debt, backed by the property itself as collateral. The mortgage appraisal serves as their assurance that the collateral is sufficient.

- Collateral Value: The appraisal provides an objective assessment of the property’s value, which is the primary collateral for the loan.

- Loan-to-Value Ratio (LVR): This ratio is a critical metric for lenders. It compares the loan amount to the property’s appraised value. A lower LVR generally means less risk for the lender.

- Risk Mitigation: If a borrower defaults on the loan, the lender can foreclose and sell the property to recover their losses. The appraisal helps ensure that the sale of the property would likely cover the outstanding loan balance.

- Compliance: Regulatory bodies often mandate appraisals for certain types of loans to ensure consumer protection and financial stability.

The Direct Impact of Appraisal Results on Your Home Loan

The outcome of the appraisal has a profound and direct effect on nearly every aspect of your home loan. It’s not an exaggeration to say that the appraisal report can make or break your financing.

The Loan-to-Value Ratio (LVR): The Core Calculation

The loan-to-value ratio (LVR) is a fundamental concept in mortgage lending, and the appraisal report is its bedrock. The formula is simple:

LVR = (Loan Amount / Appraised Value) x 100

- Example 1: You want to buy a home appraised at $300,000 and are seeking a $240,000 loan.

LVR = ($240,000 / $300,000) x 100 = 80% - Example 2: You want to buy the same home, but your offer is $320,000, and the appraisal comes in at $300,000. You still want the $240,000 loan.

LVR = ($240,000 / $300,000) x 100 = 80%

The LVR directly influences several key aspects of your loan:

- Private Mortgage Insurance (PMI): If your LVR is above 80% for a conventional loan, you will typically be required to pay PMI. This protects the lender if you default. An appraisal that comes in lower than expected could push your LVR above 80%, forcing you to pay PMI, increasing your monthly payment.

- Interest Rates: Loans with lower LVRs are generally considered less risky for lenders, often resulting in more favorable interest rates. An appraisal that significantly undervalues your home could lead to a higher LVR and, consequently, a higher interest rate.

- Loan Approval: Some loan programs have strict LVR limits. If the appraisal results in an LVR that exceeds these limits, your mortgage approval could be jeopardized.

When the Appraisal Comes in Low: Navigating the Challenges

This is often the most stressful scenario for homebuyers. When the appraised property value is lower than the agreed-upon purchase price, it creates a gap that needs to be filled. The lender will typically only loan based on the appraised value, not the contract price.

Options When Your Appraisal Comes in Low:

- Negotiate with the Seller: You can go back to the seller and present the appraisal report, requesting a price reduction to match the appraised value. The seller is not obligated to agree, but they may be willing to avoid losing the sale.

- Pay the Difference in Cash: If you have the financial means, you can cover the shortfall between the appraised value and the purchase price with your own funds. For example, if the appraisal is $280,000 and the purchase price is $300,000, you would need an extra $20,000 in cash, plus any additional down payment.

- Challenge the Appraisal: While difficult, you can request a reconsideration or a second appraisal if you believe the initial appraisal was inaccurate or flawed. This usually requires strong evidence of errors in the original report, such as overlooked comparable sales or incorrect property descriptions. Be aware that the lender will likely have to agree to a new appraisal, which can involve additional costs.

- Seek a Different Lender: Some lenders might be more flexible or have different appraisal requirements. However, this is not a guaranteed solution, as most lenders follow similar guidelines.

- Walk Away from the Deal: If none of the above options are viable or acceptable, you may have to cancel the purchase. If your purchase agreement includes an appraisal contingency, you will typically be able to get your earnest money deposit back.

When the Appraisal Comes in High: A Positive Outcome

A higher-than-expected appraisal is generally good news for borrowers, though it doesn’t always change the loan amount if you’ve already locked in a specific loan amount. However, it can offer advantages, particularly concerning your LVR.

- Lower LVR: A higher appraisal means your LVR will be lower, potentially allowing you to avoid PMI or qualify for better interest rates.

- Increased Home Equity: A higher appraised value immediately translates to greater home equity, the difference between the home’s market value and the outstanding mortgage balance. This can be beneficial for future borrowing or selling.

- Refinancing Opportunities: If you’re looking to refinance, a strong appraisal is crucial. It can help you achieve a lower LVR, potentially allowing you to refinance into a new loan with better terms or a lower interest rate, or even to cash out some of your equity.

The Appraisal in Different Home Loan Scenarios

The role of the appraisal isn’t limited to just purchasing a home; it’s also vital for existing homeowners looking to modify their financial situation through refinancing or home equity loans.

Refinancing Appraisal: Re-evaluating Your Property’s Worth

When you’re looking to refinance your mortgage, a refinancing appraisal is usually required. The lender needs to know the current property value to determine the LVR for the new loan.

- Lower Interest Rates: If your home’s value has increased since you took out the original mortgage, your LVR will be lower. This improved LVR can help you qualify for a lower interest rate on your refinanced loan, saving you money over time.

- Cash-Out Refinance: If you want to borrow more than your current mortgage balance, the appraisal dictates how much equity you can tap into. A higher appraisal allows for a larger cash-out amount.

- Debt Consolidation: Using your home equity to consolidate high-interest debts becomes more feasible with a positive appraisal.

Home Equity Loans and HELOCs: Leveraging Your Home’s Value

Similarly, when applying for a home equity loan or a Home Equity Line of Credit (HELOC), a current home valuation is essential. Lenders use this to assess the available equity in your home.

- Available Equity: Equity is the difference between your home’s current market value and the amount you still owe on your mortgage. For example, if your home is worth $400,000 and you owe $200,000, you have $200,000 in equity.

- Lender Limits: Lenders typically allow you to borrow a certain percentage of your home’s equity, often up to 80% or 85% of its appraised value, minus your outstanding mortgage balance. A good appraisal maximizes the amount of equity you can access.

Understanding Appraisal Costs and Who Pays

The cost of the mortgage appraisal is typically borne by the borrower. These are considered part of the closing costs associated with obtaining a mortgage.

Who Pays for the Appraisal?

In most home purchase transactions, the buyer pays for the appraisal. The lender will order the appraisal from a third-party appraiser as part of the loan origination process. The fee is usually collected upfront or rolled into the loan’s closing costs.

- When the Seller Might Pay: In some cases, particularly in highly competitive markets or if the seller is eager to close, they might agree to cover the appraisal cost as a concession. This is always a point of negotiation in the purchase agreement.

- Refinancing: When refinancing, the borrower requesting the refinance typically pays for the appraisal.

What are Typical Appraisal Fees?

Appraisal fees can vary significantly based on location, the complexity of the property, and the appraiser’s experience. Generally, you can expect to pay anywhere from $300 to $600 or more for a standard single-family home appraisal. More complex properties, like multi-unit buildings or those with unique features, may incur higher fees.

Navigating Lender Requirements and Appraisal Guidelines

Lenders have specific lender requirements regarding appraisals to ensure they meet industry standards and regulatory compliance.

Appraiser Qualifications

Lenders will only accept appraisals from licensed or certified appraisers who are in good standing with their state’s licensing board. These professionals undergo rigorous training and testing.

Appraisal Standards

Appraisals must adhere to the Uniform Standards of Professional Appraisal Practice (USPAP), a set of guidelines that ensure objectivity and accuracy in valuations.

Scope of Work

The appraiser’s report must include a detailed description of the property, the methodology used, comparable sales data, and a final opinion of value. The scope of work might differ slightly depending on the loan type (e.g., purchase, refinance, renovation loan).

Avoiding Appraisal Surprises: Tips for Homebuyers

While you can’t control the market or the appraiser’s opinion, you can take steps to be prepared and potentially influence the outcome.

Preparation is Key: Make Your Home Shine

Before the appraiser arrives, ensure your home is in its best possible condition.

- Clean Thoroughly: A clean and well-maintained home makes a positive impression.

- Address Minor Repairs: Fix leaky faucets, replace burnt-out bulbs, patch any holes in the walls, and ensure all doors and windows operate smoothly.

- Organize and Declutter: A tidy home appears larger and better cared for.

- Highlight Improvements: Gather documentation for any recent renovations or upgrades (e.g., receipts for new HVAC systems, kitchen remodels). This can help the appraiser identify value-adding features.

- Provide Access: Ensure the appraiser has easy access to all areas of the property, including the attic, basement, garage, and any outbuildings.

Research Comparable Sales

Before the appraisal, familiarize yourself with recent sales of similar homes in your neighborhood. Websites like Zillow, Redfin, or Realtor.com can be helpful resources. If you notice any significant discrepancies or believe the appraiser might have overlooked crucial data, you can present this information politely to the lender, who can then relay it to the appraiser.

Be Present (If Permitted)

Some appraisers allow the homeowner or their agent to be present during the inspection. If permitted, being there allows you to answer any questions the appraiser might have and point out key features or improvements that might not be immediately obvious. However, be careful not to interfere or unduly influence the appraiser.

The Appraisal in the Broader Real Estate Assessment Context

The mortgage appraisal is a specific type of real estate assessment, but it’s important to distinguish it from other property evaluations.

- Property Tax Assessment: This is conducted by local government authorities for tax purposes and may not reflect current market value.

- Broker Price Opinion (BPO): Often used by real estate agents for marketing purposes or by lenders in specific situations (like mortgage servicing), a BPO is typically less in-depth than a full appraisal.

- Home Inspection: This is focused on the physical condition of the home and its systems, identifying potential problems for the buyer, rather than determining market value.

The home valuation for a mortgage is a critical intersection of property condition, market dynamics, and financial lending requirements. It’s a process designed to provide a reliable estimate of what a willing buyer would pay and a willing seller would accept in an open market.

Frequently Asked Questions (FAQ)

Q1: How long does a mortgage appraisal typically take?

The appraisal itself, the physical inspection of the property, usually takes 1-3 hours. However, the entire process from ordering the appraisal to receiving the report can take anywhere from a few days to over a week, depending on the appraiser’s availability and the complexity of the property.

Q2: Can I choose my own appraiser?

Generally, no. To ensure impartiality and avoid conflicts of interest, lenders select the appraiser from a pre-approved list. The borrower pays for the appraisal, but the lender orders and manages the process.

Q3: What happens if the appraisal is significantly different from the purchase price?

If the appraisal is lower than the purchase price, it can impact your loan. The lender will typically only finance based on the appraised value. This may require renegotiating the price with the seller, bringing additional cash to closing to cover the difference, or potentially walking away from the deal if an appraisal contingency is in place.

Q4: How does a low appraisal affect my loan approval?

A low appraisal can lead to a higher loan-to-value ratio (LVR). If this LVR exceeds the lender’s guidelines, it could result in denial of your mortgage approval, or it might require you to increase your down payment or pay for Private Mortgage Insurance (PMI) if you didn’t initially plan to.

Q5: Can I get my money back if the appraisal is bad and I back out of the deal?

If your purchase contract includes an appraisal contingency, you can typically back out of the deal and get your earnest money deposit back if the appraisal comes in lower than expected and you cannot reach an agreement with the seller.

Q6: What are closing costs related to appraisals?

The appraisal fee itself is a direct closing cost. Other related closing costs might include fees for property inspections, title insurance, loan origination fees, and escrow fees, all of which are part of the overall expenses to finalize your home loan.

Q7: How is home equity related to appraisals?

Home equity is directly calculated using the home’s appraised value. The more your home is worth (as determined by an appraisal), the more equity you have, assuming your mortgage balance remains the same. This equity can be leveraged for loans or lines of credit.

Q8: Can I use a past appraisal for a new loan application?

Generally, lenders require a new appraisal for each new loan application. While a past appraisal might provide a general idea of your home’s value, market conditions and the property itself can change, necessitating a current real estate assessment.

Q9: What is the difference between an appraisal and a home inspection?

An appraisal determines the market value of the property for the lender. A home inspection assesses the physical condition of the property for the buyer, identifying potential defects or needed repairs. They serve different purposes.

Q10: Who is responsible for ordering the appraisal?

The lender is responsible for ordering the appraisal as part of their due diligence process for the home loan. The borrower pays for this service, but the lender manages the selection and process of the appraiser.