Yes, it is possible to get home insurance with a bad roof, but it comes with significant challenges and potential limitations. Many insurers will be hesitant to offer coverage, or may offer it with exclusions and higher premiums.

A damaged or aging roof is a major red flag for any homeowner seeking a homeowners insurance policy. Insurers assess risk, and a compromised roof significantly elevates the potential for costly claims like water damage, mold, and structural issues. This can make it difficult to secure home insurance eligibility. However, the situation isn’t always a complete roadblock. Let’s explore the nuances of navigating this complex landscape.

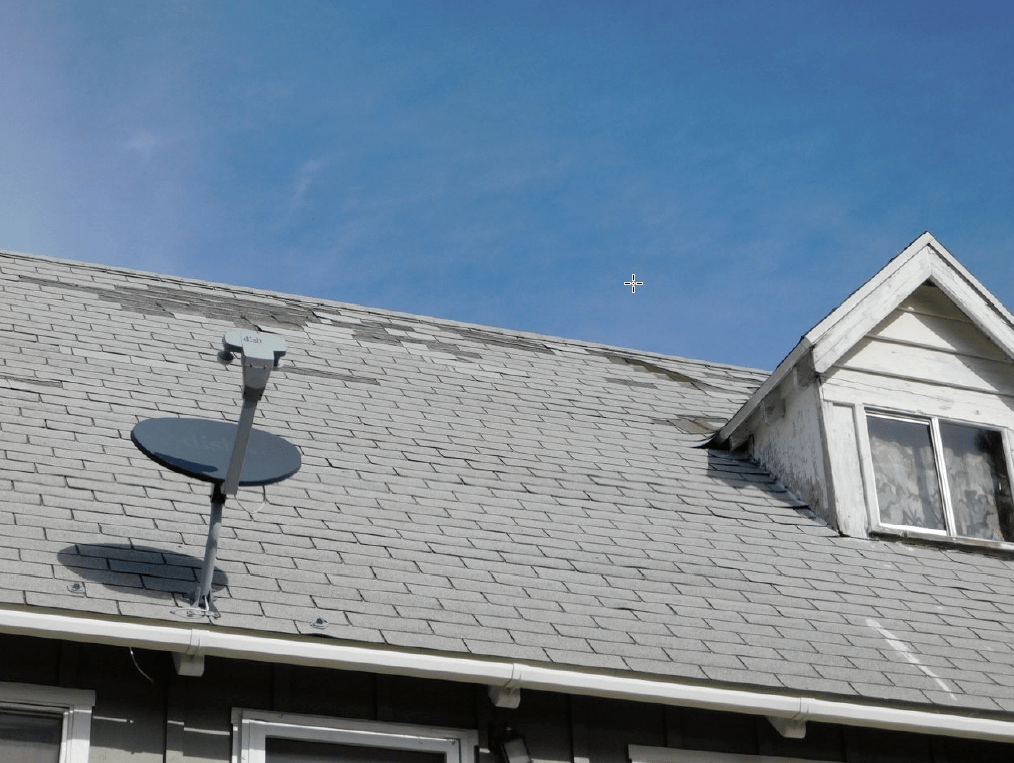

Image Source: yourgoodinsurance.com

Fathoming Insurer Perspectives on Roof Condition

Insurance companies operate on a principle of calculated risk. When they underwrite a policy, they are essentially betting that the premiums they collect will cover potential claims and leave a profit. A bad roof introduces a substantial probability of future claims.

The Significance of Roof Age and Condition

Insurers pay close attention to the age and visible condition of your roof.

- Age: Most insurers have age limits for roofs. A roof older than 20-25 years, especially if it’s asphalt shingle, may be considered at high risk. Some materials, like certain metal or tile roofs, can last longer, but age is still a factor.

- Visible Damage: Curling shingles, missing shingles, sagging sections, moss or algae growth, and water stains on the exterior or interior are all clear indicators of a roof in poor condition. These are immediate concerns for an insurer.

- Wear and Tear: Even without obvious damage, a roof that shows signs of significant wear and tear is a liability. This can include granular loss from asphalt shingles or general deterioration of the material.

How a Bad Roof Impacts Home Insurance Eligibility

A roof in disrepair can directly affect your ability to obtain insurance or the terms you receive.

- Insurer Denial: A common outcome for homes with severely damaged or very old roofs is insurer denial roof coverage. Insurers want to avoid covering pre-existing conditions that are almost guaranteed to fail.

- Higher Premiums: If coverage is offered, expect significantly higher insurance premiums roof costs. Insurers will charge more to compensate for the increased risk they are taking on.

- Specific Exclusions: You might be offered a policy, but it could come with specific exclusions related to the roof. For example, the policy might cover damage from a covered peril (like a falling tree) but not damage resulting from the roof’s poor condition (like leaks during a storm).

- Requirement for Repair or Replacement: Many insurers will only offer coverage if you agree to repair or replace the roof within a certain timeframe, typically 30 to 90 days after the policy starts.

Navigating the Maze: Strategies for Securing Coverage

While challenging, it’s not impossible to get home insurance with a bad roof. Here are several strategies to consider:

1. Honest Roof Condition Disclosure

Transparency is crucial. When applying for insurance, always be upfront about your roof’s condition. Failing to disclose known issues can lead to your policy being canceled or a claim being denied later. This falls under roof condition disclosure.

2. Seek Specialized Insurers

Some insurance companies specialize in insuring properties with higher risks. These “non-standard” or “specialty” insurers may be more willing to cover homes with older or slightly damaged roofs, though at a higher cost.

3. Obtain a Professional Roof Inspection

A reputable, independent roof inspector can provide a detailed report on your roof’s condition. This report can:

- Quantify the Damage: It provides an objective assessment, distinguishing between minor wear and tear and imminent failure.

- Estimate Lifespan: A good inspector can estimate the remaining lifespan of your roof. If it has several years left, an insurer might be more amenable.

- Identify Potential Issues: The report might highlight issues that can be addressed with relatively minor roof repair insurance rather than a full replacement, potentially making the property more insurable.

Presenting this report to potential insurers can help them make a more informed decision.

4. Address Minor Issues Promptly

If your roof has minor problems that can be fixed, tackle them before applying for insurance. Small repairs can significantly improve the perceived risk and your chances of approval. This is much more manageable than a full replacement when trying to secure home insurance eligibility.

5. Consider a “Guaranteed” or “As-Is” Policy

Some insurers offer policies that cover the structure but exclude or limit coverage for damage originating from the roof’s poor condition. This is often referred to as an “as-is” policy. While it offers some protection, it’s a compromise that leaves you vulnerable to significant costs if the roof fails.

The Cost of a Bad Roof: Premiums and Deductibles

When you do secure a policy with a less-than-perfect roof, be prepared for the financial implications.

Understanding Insurance Premiums Roof

As mentioned, insurance premiums roof costs will likely be higher. Insurers factor in the increased probability of claims. The premium might reflect:

- Age of the Roof: Older roofs naturally lead to higher premiums.

- Severity of Damage: The more significant the visible damage, the higher the premium.

- Location: Areas prone to severe weather (hail, high winds) will see higher premiums, especially with a compromised roof.

Deductibles and Their Impact

You may also encounter higher deductibles for roof-related claims. This means you’ll pay more out-of-pocket before your insurance coverage kicks in. In some cases, insurers might impose a separate, higher deductible specifically for wind or hail damage to the roof.

Claims Scenarios with a Compromised Roof

How does a bad roof affect roof damage claims? The outcomes can vary significantly.

Covered vs. Uncovered Damage

- Covered Damage: If a sudden and accidental event, like a falling tree or a severe storm, damages your already compromised roof, the insurer might still cover the repair or replacement. However, they will scrutinize the claim closely to determine if the damage was solely due to the pre-existing condition. If the insurer can prove the damage was a direct result of the roof’s poor condition (wear and tear), they might deny the claim.

- Uncovered Damage: Leaks due to old, worn-out shingles during normal rain are almost always considered wear and tear and will not be covered by a standard homeowners insurance policy. Similarly, damage from poor maintenance is typically excluded.

The Role of Insurance Underwriting Roof

The insurance underwriting roof process is where the insurer evaluates the risk. Underwriters will look at:

- Property Records: They check public records for any reported issues with the property.

- Claims History: Your past insurance claims history is a major factor.

- External Data: Some insurers use aerial imagery or data from roof condition reporting services.

- Inspection Reports: If you provide one, the underwriter will review the professional inspection report.

The underwriter’s decision is pivotal. If they deem the risk too high, they will deny coverage or offer terms that are unpalatable.

The Long-Term Solution: Roof Replacement Coverage

The most effective way to secure affordable and comprehensive home insurance is to address the roof issue head-on. Investing in a new roof is often the best long-term strategy.

Securing Roof Replacement Coverage

Once you have a new roof, obtaining roof replacement coverage is straightforward. Insurers are much more willing to cover a new, well-maintained roof. This not only improves your home insurance eligibility but also significantly lowers your insurance premiums roof costs over time.

Benefits of a New Roof

- Improved Insurability: A new roof makes you a much more attractive customer to insurers.

- Lower Premiums: You can expect to see a reduction in your insurance costs.

- Comprehensive Coverage: You’ll likely qualify for more robust coverage without exclusions related to the roof’s condition.

- Increased Home Value: A new roof is a significant investment that boosts your property’s value and appeal.

- Peace of Mind: Knowing your home is protected from the elements provides invaluable peace of mind.

Comparing Insurance Options: A Practical Approach

When dealing with a bad roof, comparing quotes from multiple insurers is essential. Here’s how to approach it:

Table: Sample Comparison of Insurers for a Home with a Compromised Roof

| Insurer Type | Potential Premium | Deductible Range (Roof Related) | Likelihood of Approval | Coverage Limitations | Notes |

|---|---|---|---|---|---|

| Standard Insurer | High | Higher than average | Low | May require roof repair/replacement within X days, exclusions | Best if roof has minor issues or is only moderately aged. |

| Specialty Insurer | Very High | High | Moderate | Often includes specific roof exclusions, limited perils | For homes with older or significantly damaged roofs. |

| Non-Standard Insurer | Extremely High | Very High | Moderate to High | Very specific exclusions, high premiums, limited coverage | Last resort for severely problematic properties. |

| Insurer after Roof Repair | Moderate to Low | Standard | High | Standard coverage, no exclusions | Ideal outcome, requires upfront investment in roof repairs. |

| Insurer after Roof Replacement | Low | Standard | Very High | Comprehensive coverage, no exclusions | Best long-term solution for insurability and cost savings. |

Important Note: The figures above are illustrative. Actual premiums and deductibles will vary widely based on location, the specific condition of the roof, the age of the home, and the insurer’s individual risk assessment.

What to Look For in Quotes

When comparing, pay close attention to:

- The exact wording of exclusions, especially those related to the roof.

- The specific deductible for roof damage or weather-related events.

- The timeframe required for roof repairs if mandated by the insurer.

- The overall coverage limits for the dwelling and other structures.

Frequently Asked Questions (FAQ)

Q1: Can I get home insurance if my roof has visible damage?

A1: It will be challenging. Many insurers will deny coverage or require you to repair the damage before they will issue a policy. Some specialty insurers might offer coverage with exclusions and higher premiums.

Q2: My roof is 25 years old. Is it too old for insurance?

A2: A 25-year-old roof is considered old for many standard insurers, especially if it’s asphalt shingles. You might face higher premiums, specific exclusions, or a requirement to replace it to qualify for coverage.

Q3: What happens if my insurer finds out my roof is in bad condition after I get a policy?

A3: If you didn’t disclose the roof’s condition during the application process, your insurer could cancel your policy or deny a claim. Honesty is the best policy.

Q4: If my roof is old, will I automatically be denied insurance?

A4: Not necessarily, but it significantly reduces your options. Insurers assess the overall risk. If other aspects of your property are in excellent condition and you can provide a professional inspection indicating remaining lifespan, you might still get coverage, albeit at a higher cost.

Q5: How can I prove my roof is in good condition to an insurer?

A5: The best way is to obtain a recent inspection report from a qualified and independent roofing inspector. This report can provide objective evidence of your roof’s state.

Q6: What is “roof replacement coverage”?

A6: Roof replacement coverage is part of your homeowners insurance policy that pays to replace your roof if it is damaged by a covered peril, such as a storm or fire, up to your policy limits. For a new roof, this coverage is typically easier to obtain and more comprehensive.

Q7: Will repairing my roof help my chances of getting insurance?

A7: Yes, absolutely. Addressing visible damage and performing necessary repairs can significantly improve your home insurance eligibility and make your property more appealing to insurers.

Q8: Are there insurers that specialize in high-risk properties, including those with bad roofs?

A8: Yes, these are often referred to as “non-standard” or “specialty” insurers. They cater to properties that don’t meet the criteria of standard insurance companies, but their policies typically come with higher premiums and more exclusions.

Q9: What is “roof condition disclosure”?

A9: Roof condition disclosure is the act of informing your insurance provider about the age, condition, and any known issues with your roof when applying for or renewing your homeowners insurance policy. It’s a critical part of the insurance application process.

Q10: How does a bad roof affect insurance premiums?

A10: A bad roof generally leads to higher insurance premiums roof costs because it increases the likelihood of claims. Insurers charge more to cover the elevated risk associated with potential damage from leaks, weather, or structural failure.

Conclusion: Proactive Measures for a Secure Future

Having a bad roof presents a significant hurdle in obtaining home insurance. Insurers view it as a major risk, often leading to denials, higher premiums, or restrictive coverage. The most reliable path forward is to address the roof’s condition proactively. Whether through timely repairs or a full replacement, investing in your roof is an investment in your home’s insurability, your financial security, and your peace of mind. By being informed, transparent, and taking necessary actions, you can navigate the complexities and ensure your home is adequately protected.