What is the taxable value of a home? The taxable value of your home is the amount of your home’s value that is used to calculate your property taxes. Can I find out how my home’s taxable value is determined? Yes, you can find out how your home’s taxable value is determined by checking your local government’s property tax records. Who determines the taxable value of my home? Your local county assessor or a similar government official determines the taxable value of your home.

This guide will help you figure out the taxable value of your home. It’s the number the government uses to decide how much property tax you owe. We’ll walk you through the whole process, step by step.

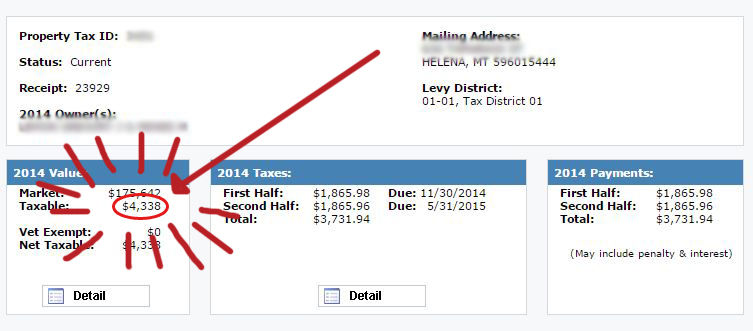

Image Source: bloximages.chicago2.vip.townnews.com

Deciphering Property Assessment

Your local government needs to know what your property is worth. This is called a property assessment. The county assessor’s office handles this. They look at many things to decide your property’s worth.

What the County Assessor Looks At

The county assessor uses several methods to figure out your property’s value. They want to get a good idea of its market value.

- Sales Comparison Approach: This is common. The assessor looks at recent sales of similar homes in your area. If similar homes sold for $300,000, your home might be worth around that.

- Cost Approach: This method looks at how much it would cost to rebuild your home today. It also considers how much value has been lost due to age or wear and tear.

- Income Approach: This is mostly used for rental properties. The assessor looks at how much income the property could generate.

Your Property Assessment Notice

You should get a notice from your county assessor’s office once a year. This notice shows your home’s assessed value. This is the value the assessor has put on your home for tax purposes. It might not be the same as the market value you could sell it for today.

Home Appraisal vs. Tax Assessment

It’s important to know the difference between a home appraisal and a tax assessment. They are not the same thing.

Home Appraisal

A home appraisal is usually done when you buy a home, refinance it, or sell it. A licensed appraiser gives an opinion of your home’s current market value. This is often for lenders to know how much the home is worth. It’s a snapshot of what a buyer might pay for it right now.

Tax Assessment

A tax assessment is done by the government. It’s for property tax purposes. The assessor tries to estimate your home’s value as of a specific date, often January 1st of the tax year. This real estate valuation might not be the same as an appraisal. It’s usually based on mass appraisal techniques, not a detailed look at your specific home.

Key Differences Summarized

Here’s a quick look at how they differ:

| Feature | Home Appraisal | Tax Assessment |

|---|---|---|

| Purpose | Buying, selling, refinancing property | Calculating property taxes |

| Performed By | Licensed, independent appraiser | Government assessor’s office |

| Value Basis | Current market value, often for a specific sale | Estimated value as of a specific date for taxes |

| Detail | Detailed inspection of the specific property | Often uses mass appraisal techniques |

Calculating Taxable Value

The taxable value of your home is the assessed value minus any exemptions you might get.

Exemptions Can Lower Your Taxable Value

Many places offer property tax exemptions. These can lower the amount of your home’s value that is taxed.

- Homestead Exemption: This is common for primary residences. If you live in your home, you might get a discount on your property taxes.

- Senior Citizen Exemption: Many areas offer this to older homeowners.

- Disability Exemption: Some places offer this for homeowners with disabilities.

- Veterans Exemption: This is for military veterans.

How Exemptions Work

Let’s say your home’s assessed value is $200,000. You have a homestead exemption that reduces your taxable value by $25,000.

- Assessed Value: $200,000

- Homestead Exemption: -$25,000

- Taxable Value: $175,000

Your property taxes will be calculated on $175,000, not $200,000.

Finding Your Home’s Assessed Value

You need to know your home’s assessed value to figure out your taxable value.

Where to Look

- County Assessor’s Website: Most county assessor offices have websites. You can usually look up your property by address or parcel number. You’ll find your home’s assessed value there.

- Property Tax Bill: Your annual property tax bill will clearly state your home’s assessed value.

- Local Government Office: You can visit the county assessor’s office in person to get this information.

What Information You’ll Need

To find your property’s assessed value online, you might need:

- Your property address

- Your property parcel number (often found on old tax bills or deeds)

Applying the Property Tax Rate

Once you know your home’s taxable value, you need to apply the property tax rate. This rate is set by your local government.

What is the Property Tax Rate?

The property tax rate is usually expressed as a millage rate or a percentage. A mill is $1 of tax for every $1,000 of taxable value.

- Example: If your taxable value is $175,000 and the property tax rate is 10 mills (or 1%), your property tax would be:

- $175,000 (taxable value) × 0.01 (tax rate) = $1,750 per year.

Local Variations in Tax Rates

Property tax rates can vary a lot from one town or county to another. This depends on local government budgets and services needed. Some areas with good schools or lots of public services might have higher tax rates.

What About Home Equity and Capital Gains Tax?

While your taxable value for property taxes is determined by the assessor, your home equity and capital gains tax are different.

Home Equity

Home equity is the difference between your home’s market value and the amount you still owe on your mortgage. It’s the portion of your home that you actually own outright. This doesn’t directly affect your property taxes. However, it’s important for selling your home or borrowing against it.

Capital Gains Tax

Capital gains tax is a tax on the profit you make when you sell an asset for more than you paid for it. If you sell your home for more than you bought it for, you might owe capital gains tax. However, there are often exemptions for the profit made on your primary residence. This is a federal tax, not a local property tax.

Appealing Your Property Assessment

If you think your home’s assessed value is too high, you can usually appeal it. This is your chance to convince the assessor that their valuation is wrong.

The Appeal Process

The steps for appealing your property assessment vary by location, but generally involve:

- Reviewing Your Assessment Notice: Carefully read the information provided by the assessor.

- Gathering Evidence: Collect information to support your claim that the assessment is too high. This can include:

- Home appraisal reports from a licensed appraiser.

- Details of recent sales of comparable homes in your neighborhood that sold for less than your assessed value.

- Photos or reports documenting any significant damage or needed repairs to your home that would lower its market value.

- Filing an Appeal: Submit an appeal form within the deadline specified by your local assessor’s office.

- Attending a Hearing: You may have the opportunity to present your case to an appeals board.

What to Present

When you appeal, focus on objective data.

- Recent Sales of Similar Homes: Show sales of homes that are similar in size, age, condition, and location that sold for less than your assessed value. This directly relates to the sales comparison approach the assessor might use.

- Your Home’s Condition: If your home needs major repairs (e.g., a new roof, foundation issues), provide documentation like repair estimates. This affects the real estate valuation.

- Appraisal Report: A professional home appraisal can be strong evidence if it supports a lower market value.

Potential Outcomes of an Appeal

- Assessment Reduced: The assessor agrees with your evidence and lowers your assessed value. This will lower your property taxes.

- Assessment Unchanged: The assessor does not agree with your evidence. You might have further options for appeal.

- Assessment Increased: In rare cases, if the assessor finds new information, your assessment could go up.

Why Accurate Taxable Value Matters

Getting your home’s taxable value right is important for several reasons.

- Fair Taxation: It ensures you pay your fair share of property taxes, no more and no less than what’s due based on your home’s value.

- Budgeting: Knowing your taxable value helps you budget for property tax payments accurately.

- Home Equity and Sales: While not directly tied, a correct assessment can sometimes reflect a more realistic market value, which can be helpful when considering your home equity or planning a sale.

- Avoiding Overpayment: An incorrect high assessment means you could be overpaying on your property taxes year after year.

Frequently Asked Questions

Q1: Is my home’s assessed value the same as its market value?

A1: Not always. Your assessed value is determined by the local government for tax purposes, often using mass appraisal methods. Your market value is what a buyer would likely pay for your home today, usually determined by a home appraisal or recent sales.

Q2: How often is my home’s property assessment updated?

A2: This varies by location. Some areas reassess properties annually, while others do it every few years. Check with your county assessor for their schedule.

Q3: What if I just bought my home? Will my property taxes go up immediately?

A3: Your property taxes are usually based on the assessment as of a specific date. If you bought your home after that date, the current owner’s assessment might still be used for that tax period. However, expect your property assessment to reflect the purchase price in the next assessment cycle.

Q4: Can I see how my neighbors’ homes were assessed?

A4: Yes. Most county assessor offices make property assessment records public. You can often view these online or at the assessor’s office to compare your home’s valuation with similar properties.

Q5: Does my mortgage payment include property taxes?

A5: Often, yes. If you have an escrow account with your mortgage lender, they collect a portion of your estimated annual property taxes with each mortgage payment and pay the taxes on your behalf when they are due.

Q6: What is the difference between assessed value and taxable value?

A6: The assessed value is the value the government places on your property. The taxable value is the assessed value minus any exemptions you qualify for. Property taxes are calculated on the taxable value.

Q7: How can I improve my chances of winning a property tax appeal?

A7: Provide strong evidence. Use recent sales of comparable properties that sold for less, get a professional home appraisal, and document any issues that reduce your home’s value. Focus on data that supports a lower real estate valuation.

By following these steps, you can gain a clear picture of your home’s taxable value and ensure you’re paying the correct amount in property taxes.